Why Asia-Pacific Day Traders Are Moving to U.S. Equities in 2026

- 5 days ago

- 2 min read

Updated: 1 day ago

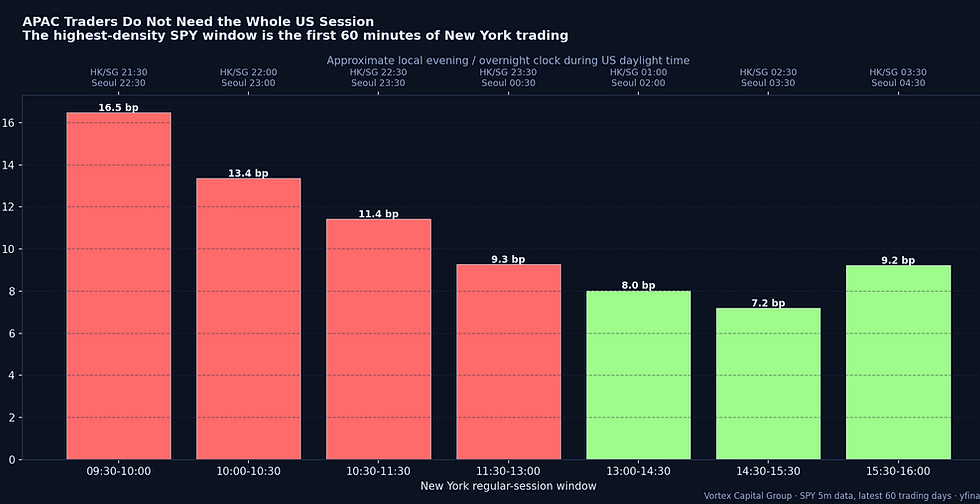

TL;DR — Asia-Pacific traders don't need to trade the entire US session. They need to convert their time-zone advantage into a structured 90-minute window: 21:30 to 23:00 local time captures the highest-edge segment of the US tape (~4× the per-minute volatility of any other window) without burning into Asian-night cognitive resources. The infrastructure question — DMA, locates, multi-clearing, real-time order flow — is what separates traders who use this window professionally from those who watch it.

APAC interest in US equities has grown sharply: deeper liquidity, more catalysts per session, broader product range, and a time-zone alignment that — for Singapore, Hong Kong, Seoul, Tokyo, Mumbai and the Gulf — places the US cash session at exactly the time their working day is ending. The misconception is that this is a marketing story. It isn't. It's a process question. The traders who treat it as a desk discipline get the time-zone benefit. The traders who treat it as "trade US whenever" burn through cash and sleep.

The handful of pieces below cover the operational specifics. This is the index post that ties them together.

Region-specific playbooks

Singapore / Hong Kong: turning the 21:30 open into a repeatable desk routine — SPY 4× per-minute volatility lands at 22:30 HKT/SGT in winter.

Hong Kong dual-listings: 9988.HK ↔ BABA opening dislocation — β = 0.45–0.71, US makers under-react to HK momentum.

Mainland China: CSI 300 → US-open 6-hour window — A-share momentum reverses in US session.

China execution infrastructure: what Chinese day traders need to know.

Seoul / Korea: KOSPI close → SPY gap fill, first-5-min reversal manual, and the Seoul → NY semis bridge.

Gulf (Dubai / Riyadh): Sector-Gate ORB for the 18:15 Dubai window.

Why the desk infrastructure determines whether the time-zone helps

APAC traders compete with retail flow that's been internalized through wholesalers and with institutional desks that route through DMA. The trader sitting in Hong Kong at 22:30 HKT making a directional call on NVDA has the same chart everyone else has. What separates them is whether the order arrives at the venue that matches the trade's intent. Our DMA vs Retail Broker Execution piece quantifies the per-window cost surface. The PFOF Tax piece covers why zero commission isn't zero execution cost.

What APAC traders should actually evaluate

DMA + multi-venue smart routing (not retail order tickets) — see the DMA piece for the per-window math.

Multi-vendor HTB locate access for shorts on names like UPST, BYND, AMC, TLRY, GME — see Four HTB Vendors.

Real-time order flow stack (CVD, VWAP, heatmap, ladder) — not delayed retail feeds.

Multi-clearing redundancy for margin, locate and routing flexibility — see Multi-Clearing Access.

Joining the desk

If you're an APAC-based active trader and your evening process already includes pre-market scanning, locate confirmation, and a written route plan before the bell — our trader application takes about ten minutes; every serious candidate hears back within five business days.

Comments