Trading U.S. Equities from China: Infrastructure, Platform Access, and What Serious Day Traders Do Differently

- 5 days ago

- 2 min read

Updated: 1 day ago

TL;DR — China-based traders don't need a simplified gateway to US stocks. They need a professional execution stack — DMA, Sterling Trader Pro, multi-vendor HTB access, real-time order flow, multi-clearing. The Beijing-time advantage (US open lands at 21:30) is structural, not lucky. Whether it converts to P&L depends on whether the trader's order path can compete with the institutional flow that's been waiting for the bell.

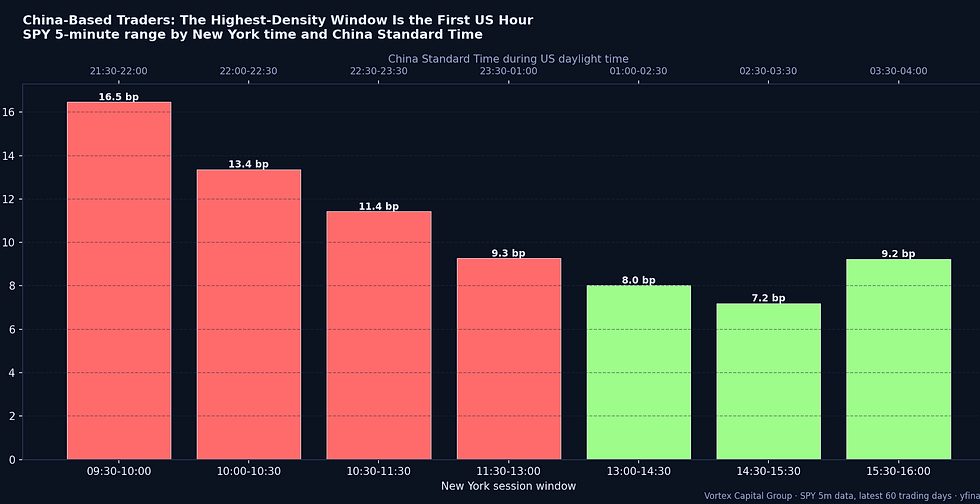

This post overlaps deliberately with our deeper US 日内交易基础设施 piece (Simplified Chinese). This English version is the hub for English-readers based in or working with the China market. The Chinese-language piece carries the timing data (SPY 4.8 bp/min at 22:30 Beijing vs 2.3 bp at 03:30) and the local routine. This piece covers the broader execution question.

What Chinese traders actually need beyond the chart

DMA, not retail routing. Our DMA vs Retail Broker piece shows where retail routing surrenders the most edge during the day's high-volatility windows.

Multi-vendor HTB access. China ADRs like BABA, JD, PDD often see borrow stress during news/earnings windows. Four HTB Vendors covers why a single vendor is a single point of failure.

Real-time order flow. CVD, VWAP, heatmap, price ladder — these tools are how the desk separates participation from sponsorship. Our Volume Shock study demonstrates the difference.

China ADR cross-session reads. The CSI 300 → US-open 6-hour window quantifies how A-share momentum REVERSES in the US session — counter to the textbook reading.

Multi-clearing redundancy. Borrow, margin, and route choice all improve with more than one clearing relationship — see Multi-Clearing Access.

The cross-market reads that matter

China-based traders have one of the cleanest informational positions in global equities: A-share session, HK session, then US session in sequence. The China ADR Playbook covers BABA / NIO / JD / PDD / KWEB cross-market behaviour. The Hong Kong dual-listing study covers the β < 1 makers' under-reaction. The CSI 300 → US window piece covers how A-share momentum actually inverts intraday in the US.

These aren't theoretical. They're the cross-session reads our desk runs every evening — and they only convert to P&L if the execution stack can act on them at 21:30 Beijing without burning the edge to spread.

Joining the desk

If you're a China-based active trader and you already think in cross-session terms — A-share to HK to US — our trader application takes about ten minutes.

Comments