Volume Shock Without Sponsorship: The Exhaustion Edge

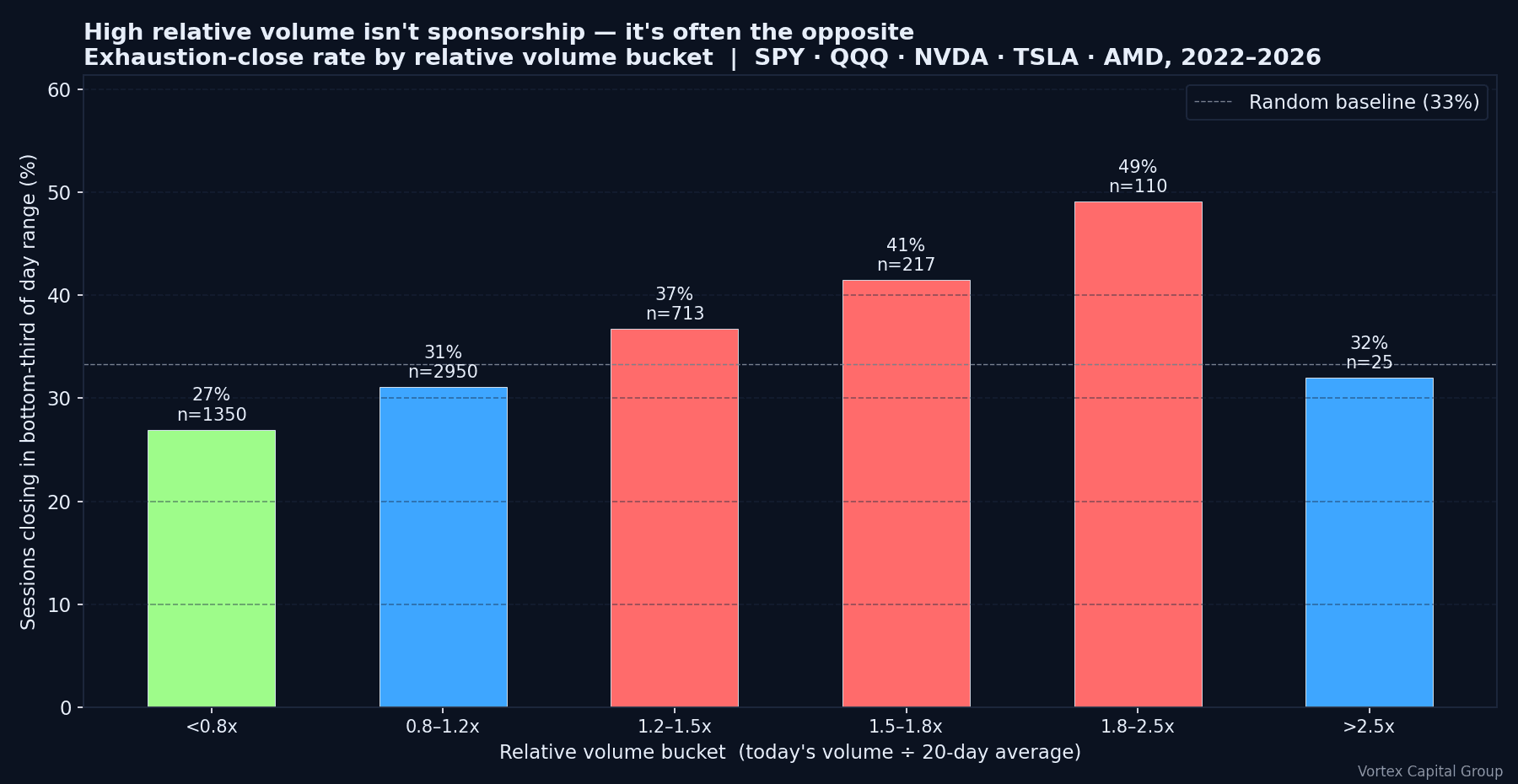

TL;DR - High relative volume is not automatically institutional demand. Across 5,365 sessions on SPY, QQQ, NVDA, TSLA and AMD since 2022, the rate of "exhaustion close" - close in the bottom third of the day's range - climbs monotonically from 27% at calm volume (<0.8× the 20-day average) to 49% at 1.8-2.5× volume. The exception is the extreme >2.5× bucket (32%), where volume is usually catalyst-driven and price holds. Volume is participation. Sponsorship is something else, and the order book tells us which we're looking at.

Volume is the easiest institutional-looking signal to misread. A stock trading 1.8× normal volume can be under accumulation, under distribution, or simply under stress. We aren't paid for noticing activity. We're paid for identifying who still has control after the activity appears. The first spike tells us a lot of orders ran. It doesn't tell us who's left holding.

What 5,365 sessions actually show

The chart below quantifies the relationship between relative volume and end-of-day price location across our liquid-name universe. "Exhaustion close" is defined as the session closing in the bottom third of the day's high-low range. Higher rate = more sessions where heavy volume produced a poor close.

Read the table line by line and the playbook writes itself:

- Below 0.8× relative volume: exhaustion-close rate 27%, below the 33% random baseline. Calm tape, controlled distribution - these aren't the sessions to fade.

- 1.5-1.8× relative volume: exhaustion rate 41%. The danger zone. Heavy enough to look like institutional demand, light enough that the moves frequently reverse. This is where retail accounts confuse participation with sponsorship most often.

- 1.8-2.5× relative volume: exhaustion rate 49%. Coin-flip territory at the bar level, but the asymmetry is unmistakable when overlaid with VWAP and CVD context. Without sponsorship confirmation, this bucket is statistically a fade window.

- Above 2.5× relative volume: exhaustion rate drops to 32%. These are the genuine catalyst sessions - earnings, M&A, FDA decisions, regulatory news. Real flow is in the tape and the move usually holds.

Participation is not sponsorship

Participation means people are trading. Sponsorship means better-capitalized or persistent participants are still willing to support the move after the first impulse. A stock can print huge volume because shorts are covering, market makers are hedging, retail traders are chasing, index baskets are rebalancing, or stops are getting triggered in chains. None of that is sponsorship. The question is whether anyone with conviction is still bidding once the first wave clears.

This is why the close of the impulse bar matters more than the size of it. Volume surges and the candle closes near the low - participation didn't translate into acceptance. Volume surges, price holds above VWAP, and CVD keeps expanding after the pullback - the move has a better right tail. The data above is just the macro view; the trade decision lives in the next ten minutes after the surge.

The sponsorship checklist

- CVD should expand with price, not flatten while the candle keeps making new highs. Divergence at high relative volume is the first clue demand is weakening.

- VWAP should be accepted after the first impulse. A quick reclaim that fails is a warning, not an automatic dip-buy signal.

- Displayed depth should refresh after impact. If liquidity vanishes after every marketable order, we size down or pass.

- Dark-pool prints are context, not prophecy. A large print near the high matters more when the lit book can't continue higher afterward - and matters less in isolation.

How exhaustion forms before the reversal candle

Most reversal candles are late evidence. Exhaustion usually starts several minutes earlier. Price pushes to a new high, but the bid stops refreshing. Spreads widen on every new print. Aggressive buyers keep lifting offers, yet the stock can't extend. Then a small downtick travels farther than expected because the supporting book is hollow. The reversal candle is the print that finally pays out a structure that's been weakening for ten bars.

Our desk watches the relationship between impact and repair. A sponsored move takes liquidity and repairs quickly - buyers keep stepping in. An exhausted move takes liquidity and leaves a hole. That hole is the opportunity, but only if the trader can define risk. Fading volume shocks without a risk plan is more expensive than chasing them.

Where short access matters

If the name is easy to borrow, the fade can be expressed with clean timing. If it's hard to borrow, the trade may not be available to retail accounts at the moment the setup appears. Our locate desk maintains four-vendor HTB access precisely so this isn't a constraint. We covered the mechanics in detail in our hard-to-borrow infrastructure piece.

A practical tape drill

Before the open, pick three names with expected relative volume above 1.5× and write down the exact condition that would prove sponsorship. For one name, that may be a VWAP hold after the first pullback. For another, a higher low with CVD continuing to rise. For a third, the ability to absorb a 30-second wave of offers without breaking the level. The pre-trade definition prevents post-trade rationalization.

During the first 15 minutes, score each name on three questions. Did price hold above the level where volume first appeared? Did aggressive buying produce higher prices, or only prints into supply? Did the book repair after impact, or did liquidity disappear underneath the move? Two clean answers earn participation. One ambiguous answer earns a pass.

After the trade, review the same three variables instead of judging only P&L. The useful journal note isn't "volume spike failed." It's "volume spike failed because CVD flattened on the second high, VWAP acceptance never developed, and refreshed liquidity appeared on the offer inside 30 seconds."

Related

Volume-shock exhaustion is one read of a broader regime. We also covered VIX-driven range expansion, yield-shock sector behaviour, and the 10:30 VWAP decision point - each is a different way to ask the same question: does the move have sponsorship or only participation?

How we trade it on the desk

Vortex Flow gives us the missing context - CVD, VWAP, heatmap liquidity, price-ladder behaviour, and whether aggressive activity is producing real acceptance. DMA through Sterling Trader Pro gives the order control to choose passive participation, marketable limits, smart routing, or no trade at all. Locate infrastructure makes the short side available when the setup is symmetric. We want applicants who can describe the difference between participation and sponsorship before asking for size. Our trader application takes about ten minutes.

#VolumeShock #OrderFlow #CVD #VWAP #DayTrading #ExhaustionClose #PropTrading #HardToBorrow #DMA #RelativeVolume #VortexCapitalGroup

Trade with the desk behind the research

Vortex Capital Group gives qualified traders DMA via Sterling Trader Pro, multi-vendor HTB locates, smart and dark-pool routing, and an 80%+ monthly profit share.

Apply to Trade