Risk-Off Equity Routing: How VIX Spikes Reprice SPY & QQQ

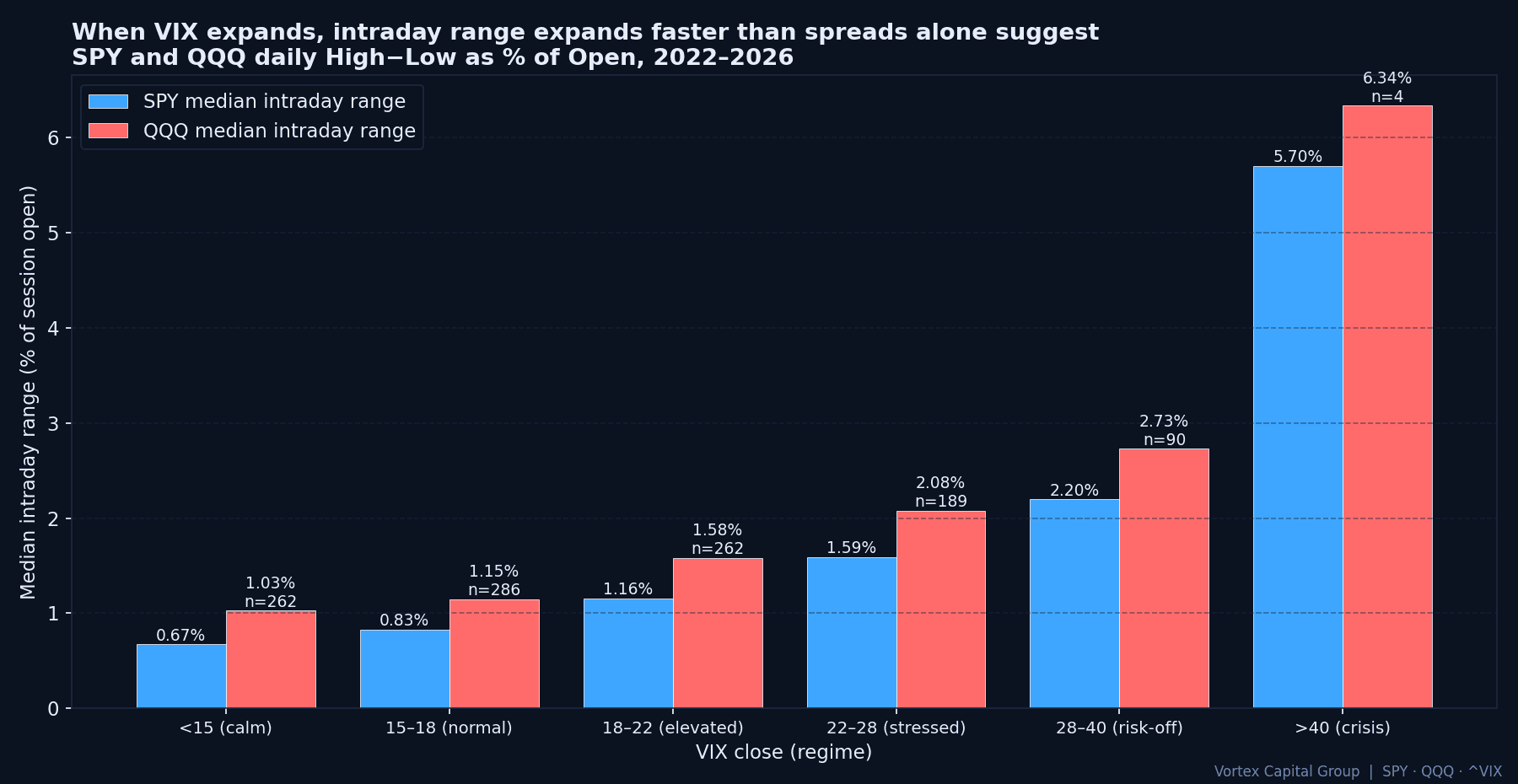

TL;DR - On the 90+ trading days where VIX closed above 28 since 2022, the median intraday range on SPY widened to 2.20% and QQQ to 2.73% - roughly 3× the calm-tape median (0.67% and 1.03% under VIX 15). Spreads widen, displayed depth gets less reliable, and the route choice carries more P&L impact than the directional call. We don't trade risk-off sessions by cutting size and hoping spreads behave. We reprice three inputs - volatility, ETF volume, and quote stability - and let those decide the route, not the chart.

A risk-off tape isn't just a bearish tape. It's a liquidity regime. Index hedges flow through ETFs, basket rebalances accelerate, market makers widen quotes, and displayed depth turns less reliable at exactly the moment traders demand immediacy. The trader who uses a normal-session order style on a stressed tape stops earning edge from the chart and starts donating it to the route.

Our desk separates direction from liquidity. Direction says whether we want long, short, or no exposure. Liquidity says whether the trade can be expressed cleanly. A name can have a textbook short setup and still be a poor trade if the spread has doubled, the inside quote is unstable, and the dark venues are quiet. The setup is real; the route makes it tradeable.

What the data says about range expansion

Before talking framework, here's the underlying behaviour we're trading against. The chart below shows median intraday range - measured as (High - Low) ÷ Open - across SPY and QQQ from 2022 to 2026, bucketed by daily VIX close.

Range roughly triples from VIX <15 to VIX 28-40, and roughly sixfolds at VIX >40. Spread widening is part of that picture but only part - quote life shortens, retail flow exits, and the participants left in the book have shorter time horizons. The same marketable order that costs 1-2 bp on a calm tape costs 5-10 bp on a risk-off tape before any directional risk is even taken.

The three inputs we reprice first

Volatility. When VIX expands, the market is charging more for certainty. The same marketable order that was acceptable in a calm tape gets expensive in a stressed one - wider quoted spread, shorter quote life. Above VIX 22, we stop assuming any quote we see has another second of life.

ETF volume. If SPY, QQQ, IWM or the sector ETFs are running well above their 20-day average volume, the market is being driven by basket flow, not single-name conviction. That changes how much weight we give to single-name technicals - a clean short setup in a single semi name during a 2× SMH volume session is mostly a bet on the basket, not the name.

Quote stability. Displayed size on the top of book can be a lie. If the inside quote refreshes after every print, we have a stable book. If it flickers - size appears, gets cancelled when challenged, reappears at a worse level - the book is unstable and passive orders earn nothing. In that state, hidden routes and ATS interaction are usually the better path. We covered the venue logic in detail in our dark-pool liquidity study.

Those three inputs determine the route. A tight-spread normal tape lets us take passive entries, midpoint attempts, or patient scaling. A risk-off tape forces a cleaner decision: the trade deserves urgency with a hard limit, or it doesn't deserve participation. The middle ground - passive orders sitting on a flickering book during a stress event - is where retail accounts donate the most edge.

ATS awareness during stress

ATS and dark-aware routes help most when footprint is the main cost. In a stressed tape, hidden liquidity gets judged against opportunity cost. If the market is repricing every few seconds, waiting for midpoint interaction is a polite way to miss the trade. If the name is liquid and the move has confirmation, hidden routes still work, but the cost of waiting is now measured in basis points per second, not per minute.

We watch whether ETF pressure is leading or confirming the single name. If a semiconductor stock breaks while QQQ and SMH are also expanding lower, the route can carry more urgency because market-wide pressure supports the move. If the single name is moving against the basket, we treat it as idiosyncratic information and accept that hidden order types might be the only acceptable expression.

Our risk-off routing playbook

- Spread widening + fast setup → controlled urgency with a hard limit, or we don't trade. Undefined urgency is not allowed.

- ETF volume confirms direction → less patience on entries, but the single name must hold VWAP or a key liquidity level.

- Displayed depth flickers → passive orders lose value. We move to hidden, ISO, or peg-to-mid via ATS routes.

- Basket-driven move → we don't pretend every single-name wick is stock-specific information. The trade is the basket, not the chart.

The most useful post-trade question on a risk-off day isn't whether the idea worked. It's whether the order style matched the regime. Did we pay for immediacy when the trade didn't need it? Did we wait for hidden liquidity when the tape demanded action? Did we size based on a normal spread even though the market had moved to a different regime two hours earlier? The answers separate consistent risk-off P&L from sessions where the directional call was right but the route ate the move.

Related: how we read the same regime through other lenses

Risk-off doesn't only show up in VIX. The yield-shock playbook covers how the same regime registers in QQQ, NVDA and SMH when Treasury yields move. The volume-shock study quantifies how often heavy relative volume is sponsorship versus exhaustion - a daily question on stressed tapes.

How we're built for it

Vortex Capital Group's qualified traders run DMA through Sterling Trader Pro, with multi-venue smart routing, ATS awareness, locate infrastructure across four HTB vendors, and the Vortex Flow + Vortex Edge stack for real-time order-flow context. Risk-off sessions expose weak execution stacks fastest. We want traders who can explain route choice before they explain chart bias. If that's you, our trader application takes about ten minutes - every serious candidate hears back within five business days.

#RiskOff #VIX #ETFVolume #ATS #DarkPools #DMA #SmartRouting #ExecutionQuality #SPY #QQQ #PropTrading #VortexCapitalGroup

Trade with the desk behind the research

Vortex Capital Group gives qualified traders DMA via Sterling Trader Pro, multi-vendor HTB locates, smart and dark-pool routing, and an 80%+ monthly profit share.

Apply to Trade