Opening Range Breakout: A Statistical Framework for Active Equity Day Traders

- 4 days ago

- 5 min read

Updated: 1 day ago

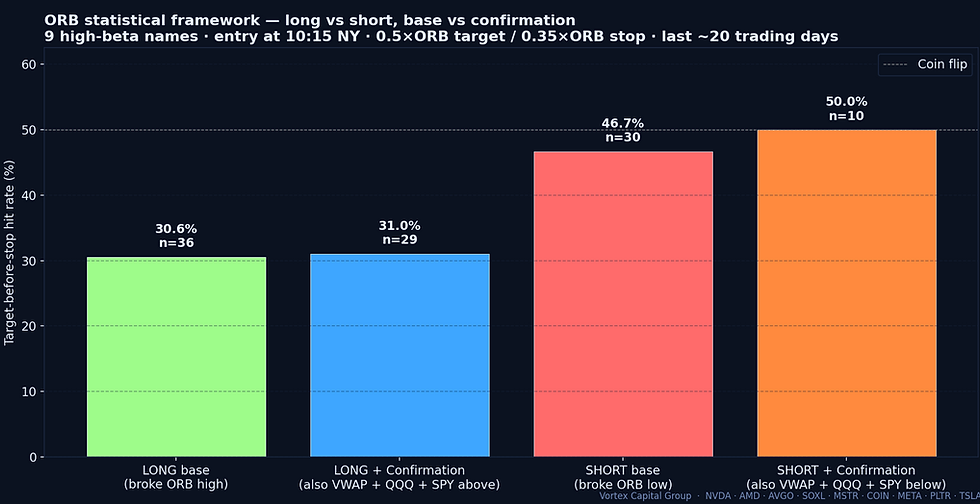

TL;DR — This is the desk framework that sits above our 09:30–09:45 study. Across the last 20 trading days on 9 high-beta momentum names (NVDA, AMD, AVGO, SOXL, MSTR, COIN, META, PLTR, TSLA), the data has inverted from what the framework historically assumed: long ORB hit rate is 30.6% baseline, 31.0% with VWAP + QQQ + SPY confirmation; short ORB is 46.7% baseline, 50.0% with full confirmation. In the current regime, short-side breaks are the higher-probability trade. The framework's value isn't a fixed hit-rate target — it's the discipline to apply confirmation, route control and post-trade review regardless of which side the regime favors.

Opening Range Breakout is easy to describe and hard to trade well. Mark the first range, buy the high, short the low, place a stop on the other side. That version is a chart pattern. Our desk treats ORB as an auction test: did the first 15 minutes establish a participation level the rest of the day will defend, or did the range form by accident around the opening imbalance?

This post is intentionally different from our canonical 09:30–09:45 ORB research note. That post measured which opening-range breaks followed through. This is the operating framework: when we participate, when we pass, when the route matters more than the signal, and why long-side and short-side ORB rarely share the same threshold.

The current framework test — what the data says now

We tested the last ~20 trading days on nine liquid momentum and index names. Entry is evaluated at 10:15 ET if price has broken above the opening high or below the opening low. Target = 0.5×ORB, stop = 0.35×ORB. Four findings, two of which invert the framework's historical assumption:

Long base ORB: 30.6% target-before-stop (n=36). Substantially below the 50% the framework historically assumed. The current regime is not rewarding long-side breakouts cleanly.

Long ORB with full confirmation (VWAP + QQQ + SPY all above): 31.0% (n=29). Confirmation barely improves the rate — a sign that the regime, not the filter, is the limiting factor.

Short base ORB: 46.7% (n=30). Materially higher than historical short-ORB baselines. In a tape where rallies are crowded and reversals are sharp, the downside break is doing the work.

Short ORB with full confirmation: 50.0% (n=10). Small sample, but the confirmation filter pushes hit rate to coin-flip — and the absolute risk-reward is positive (0.5×ORB target vs 0.35×ORB stop).

The honest read: a framework that hard-codes "longs are easier than shorts" was built for the 2020-2023 trend regime and isn't describing the 2025-2026 regime. The framework's principles still hold (confirmation > raw signal, route discipline matters, longs and shorts are not mirror images), but the empirical asymmetry has flipped direction. Traders who default to long-ORB-only in this tape are giving up the high-probability side of the setup.

The four questions before any ORB entry

1. What created the first range? A range built by catalyst participation is different from a range built by one opening imbalance. We want to know whether the pre-market range had tradable liquidity, whether the stock is crowded, and whether the opening 15 minutes look like genuine demand or a reflex print.

2. Is VWAP accepted or only touched? A break that immediately loses VWAP is not the same as a break that pulls back, holds VWAP, and attracts a second wave of participation. We care more about acceptance after the first impulse than the first impulse itself. The 10:30 VWAP Decision Point covers this in σ-distance terms.

3. Does the basket agree? For momentum names, QQQ and SPY confirmation change the quality of the trade. A stock breaking higher while the index basket is above VWAP is a different auction from a stock breaking alone against a weak tape. In current data, basket confirmation matters more on the short side than the long side — see the chart above.

4. Can the order be executed without donating the edge? ORB often appears when spreads are wide and traders are impatient. A valid signal can still be a bad trade if participation requires crossing a poor spread or chasing a flickering book. The PFOF Tax piece quantifies how a few basis points of route drag erase short-target setups specifically.

Why short ORB needs a higher bar — and why that bar is currently being met

Short ORB has traditionally needed a stricter checklist. A stock can break the opening low because the first buyers are done, because a basket is under pressure, because borrow is tightening, or because stop orders were swept into a temporary low that immediately reverses. Each cause carries a different expected path.

Our short-side ORB checklist is stricter regardless of current hit rates: borrow must be confirmed before the trigger (see HTB Mechanics), the stock must stay below VWAP after the first retest, QQQ or the relevant sector ETF should confirm, and Vortex Flow must show that sellers are getting filled rather than absorbed. In the current regime, this checklist is producing 50% hit rates with positive risk-reward — but the checklist is what makes the trade clean even when the regime turns.

The failed-break pattern we avoid

The most expensive ORB failure looks good for about ninety seconds. Price breaks the opening high, spreads widen, late traders cross the offer, and CVD stops expanding as the candle extends. Then price loses VWAP or returns into the range while the late longs hold inventory they paid the worst price for. In the current regime, this is exactly the long-ORB failure mode driving the 30% base rate.

The cleaner setup is slower: break, controlled pullback, VWAP hold, second push with better flow than the first. That's when route choice matters. Sometimes the route needs lit urgency; sometimes the better trade is passive on the retest. The Smart Routes vs Manual Routes piece covers when to override the smart router.

Execution is part of the signal

ORB entries happen in a high-cost liquidity window. That's why we connect Vortex Edge scans, Vortex Flow confirmation, Sterling Trader Pro hot keys, and DMA route choice into one workflow. If the only way to enter the breakout is to accept poor fills, the trade has already lost some of its expected value before it begins.

This is where execution content connects directly to the ORB framework. The PFOF Tax explains why small route drag matters when the target is measured in fractions of the opening range. Dark Pool Liquidity explains when hidden or midpoint interaction is worth the wait. The DMA vs Retail Broker piece covers the per-second cost of latency.

Desk operating rules

No pre-market map, no ORB trade. We need catalyst, range, volume, spread, and borrow context before the bell.

No VWAP acceptance, no size. A break without acceptance is a sweep, not a trend.

Longs and shorts do not share the same threshold — and the dominant side rotates by regime. Right now, short ORB is statistically the better trade on this universe. Treat that as data, not bias — and re-measure quarterly.

Route choice is written before entry. Urgent, passive, midpoint, smart route, or no trade must be decided before the trigger.

Review fills, not just candles. A losing ORB with a clean route is a strategy review. A winning ORB with a sloppy fill is still an execution problem.

Related reads

The 09:30–09:45 Auction (canonical study) · Gulf Sector-Gate ORB (regional variant) · 10:30 VWAP Decision Point · PFOF Tax · Smart Routes vs Manual Routes.

Join the desk

We want ORB traders who can define invalidation before entry, explain the order-flow confirmation, and describe why the selected route matched the trade. If your process is built around auction context, flow confirmation, and execution review — and you can update your assumptions when the regime turns — the trader application runs about ten minutes.

Comments