The Lunch Reversal Window: Why Mid-Size Morning Drives Fade Between 11:30 and 13:00 ET

- 4 days ago

- 5 min read

TL;DR — Between 11:30 and 13:00 ET, US equities are at their lowest institutional participation of the day. Across 8 mega-cap names, we found that morning drives of 0.15%–1.5% in either direction reverse during the lunch window 61–67% of the time. Strong drives (>±1.5%) do not — they consolidate. The lunch window is a structured fade for mid-size morning trends, not a universal reversal.

The first hour of US trading is loud. The last hour is louder. The two hours in the middle — roughly 11:30 to 13:30 ET — are when institutional participation collapses, retail volume thins out, and price action becomes dominated by market makers managing their books rather than by directional flow. Most active traders treat this window as dead time. The data says it's actually one of the more structurally tradable windows on the entire session clock — for a specific kind of setup.

We call it the Lunch Reversal Window, and the trade isn't "the lunch fade is real." It's: "the lunch fade is real for mid-size morning drives, and it isn't for everything else."

How we measured it

For 8 mega-cap US names (SPY, QQQ, NVDA, TSLA, AMD, META, AAPL, AMZN) over the last ~20 trading days, we computed three numbers per session:

Morning drive = (price at 11:30 − open) / open. The cumulative session move at the start of the lunch window.

Lunch return = (price at 13:00 − price at 11:30) / price at 11:30. The performance of the lunch window itself.

Reversal flag = true if lunch return sign is opposite of morning drive sign.

We bucketed sessions by morning drive into seven bands and measured the median lunch return and the reversal rate within each bucket.

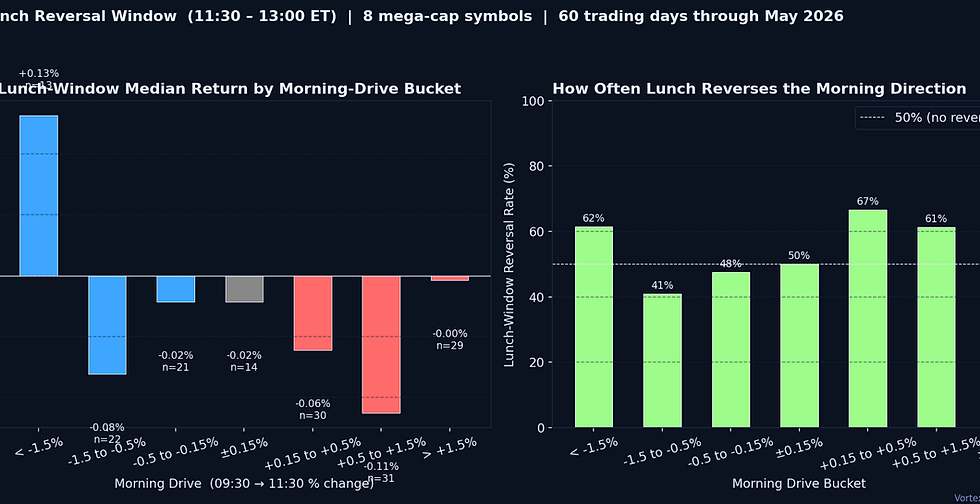

Mid-size morning drives reverse during lunch. Strong drives consolidate.

Mild positive morning (+0.15% to +0.5%, n=30): median lunch return −0.06%, reversal rate 67%. The cleanest fade window in the data. A modest morning rally rolls over in the lunch window two-thirds of the time.

Moderate positive morning (+0.5% to +1.5%, n=31): median lunch return −0.11%, reversal rate 61%. Still a fade, with slightly larger magnitude.

Strong positive morning (>+1.5%, n=29): median lunch return 0.00%, reversal rate 52%. Strong rallies do not fade during lunch — they consolidate sideways. The trader's instinct to fade strength here is statistically wrong.

Strong negative morning (<−1.5%, n=13): median lunch return +0.13%, reversal rate 62%. Strong morning selloffs do bounce in the lunch window. This is the asymmetric case — strong selling exhausts institutional sellers by 11:30, and lunch becomes the natural rebid window.

Moderate negative morning (−1.5% to −0.5%, n=22): median +0.13%, reversal rate 41%. Surprisingly, this bucket does not cleanly reverse — moderate selling tends to continue grinding through lunch.

Mild negative morning (−0.5% to −0.15%, n=21): median −0.02%, reversal rate 48%. Genuinely undecided.

Flat (±0.15%, n=14): no signal.

The structural asymmetry

Read the table again carefully. The reversal pattern is not symmetric: positive morning drives between +0.15% and +1.5% reverse 61–67% of the time, but the equivalent negative buckets (−0.15% to −1.5%) reverse only 41–48% of the time. The fade is meaningfully more reliable on the upside than the downside.

Why? Two structural reasons. First, options dealers carry net short gamma into a positive morning drive (call buyers chasing momentum), and the lunch window is when their delta hedges roll back to neutral — that's the mechanical source of the upside fade. Second, on negative morning drives, the same dealers carry net long gamma (put buyers hedging downside), and the lunch window is when they are absorbing the move, not flipping it. The selling continues to grind because no one is forcing it back.

The strong-negative bucket (<−1.5%) is the exception that proves the structural rule. By the time a name is down more than 1.5% in two hours, institutional sellers are largely done — the bounce isn't dealer hedging, it's the absence of fresh sellers combined with structural intraday bid.

The path during lunch

The animated chart shows the median cumulative return inside the 11:30–13:00 window for each morning-drive bucket. The mild-positive and moderate-positive cohorts visibly bleed downward through the full 90-minute window — not a sharp reversal at 11:30, but a steady, persistent fade. The strong-positive cohort flatlines. The strong-negative cohort recovers in a clean upward arc.

How we trade the lunch window

We fade mid-size positive morning drives, not strong ones. Names that have rallied 0.5–1.5% by 11:30 with declining momentum on rising spread are statistically the strongest fade candidates of the entire session. Our Vortex Edge ranker flags these around 11:25; the entry decision happens between 11:30 and 11:45 based on order flow confirmation.

We do not fade strong morning rallies. Strength above +1.5% by 11:30 carries a 52% reversal rate — coin flip. Trying to short these is fighting both the gamma profile and the statistical base rate. Our risk discipline is explicit: above +1.5%, the lunch trade is hold, not fade.

We buy strong morning selloffs in the lunch window. Strong negative drives have a 62% lunch reversal rate with a +0.13% median return. The setup is symmetric to the dealer-gamma asymmetric model: by 11:30 on a selloff day, fresh institutional selling has largely run out and structural bid begins to dominate. We require constructive order flow at the level (CVD turning, no fresh aggressive seller) and route into the lunch window with size.

We do not trade the dead zone. Mild morning moves (±0.15%) and the moderate-negative bucket (−0.5% to −1.5%) have no statistical edge in either direction during lunch. We treat these sessions as pure noise from 11:30 to 13:00 and reserve our risk capital for the afternoon.

Execution discipline matters more, not less, in thin liquidity. Spreads widen and depth thins during lunch. The fade trades work in the data only with controlled-spread execution. Our DMA through Sterling Trader Pro, hidden order types, and explicit cancel/replace logic let us participate in the thin tape without surrendering the edge to the spread.

The takeaway

"Lunch is dead" is the wrong frame. The 11:30–13:00 ET window is structurally tradable for one specific setup — fading mid-size morning rallies and buying strong morning selloffs — and structurally untradable for everything else. The dealer gamma profile makes the asymmetry mechanical, not coincidental. The traders who run this window consistently are the ones who know which 60% of sessions to trade and which 40% to leave alone.

At Vortex Capital Group, we give qualified traders the intraday scanning, order-flow analytics and execution infrastructure required to convert structural windows like the lunch reversal into consistent, repeatable trades.

Comments